The $9 Billion Secret: How One Lawyer Exposed Chase’s Fraud

Alayne Fleischmann kept a heavy secret for eight years. A securities lawyer with sharp instincts and a background in human rights work, she witnessed what she later described as “massive criminal securities fraud” inside one of the world’s most powerful financial institutions. The burden of that knowledge was immense. “It was like watching an old lady get mugged on the street,” she said of the experience. “I thought, ‘I can’t sit by any longer.'”

Fleischmann is the central figure in a narrative that exposes the dark underbelly of the 2008 financial crisis and the subsequent failures of the American justice system to hold top executives accountable. She possesses the secrets that JPMorgan Chase CEO Jamie Dimon paid a staggering sum to keep hidden from the public eye. While headlines touted a record-breaking $13 billion settlement, the reality was a negotiated peace treaty that allowed the bank to purchase silence, burying the evidence of systemic corruption deep within a “Statement of Facts” that obscured more than it revealed.

The story of the JPMorgan Chase settlement is not just a tale of financial malfeasance; it is a case study in the architecture of a cover-up. It reveals how a major bank, with the tacit cooperation of the Department of Justice, managed to bypass the court system, avoid criminal charges for its leadership, and leave the American taxpayer to foot the bill for its deceit. For anyone witnessing corporate wrongdoing today, Fleischmann’s ordeal serves as both a cautionary tale and a rallying cry for the vital importance of whistleblower protection.

The Mortgage Meat Grinder

In 2006, Fleischmann was working as a transaction manager at JPMorgan Chase. The housing market was overheating, and banks were in a frenzy to buy pools of home loans and repackage them as mortgage securities. These financial products were then sold to pension funds, insurance companies, and other institutional investors. Fleischmann’s role was essentially quality control; she was the gatekeeper tasked with ensuring the bank didn’t buy “spoiled merchandise.”

However, the culture at Chase had shifted aggressively against transparency. Fleischmann encountered immediate resistance from a new diligence manager who implemented a bizarre and alarming policy: employees were told to stop sending him emails. In the compliance world, where a paper trail is the only defense against liability, a “no email” edict is a screaming siren indicating intent to hide information. If an employee violated this rule, they were verbally reprimanded. The objective was clear—do not create a record of the rot inside the machine.

The rot was undeniably there. In late 2006, Fleischmann’s team reviewed a package of loans from a mortgage originator called GreenPoint, valued at roughly $900 million. These weren’t prime mortgages. They were what the industry called “scratch and dent” loans—mortgages that had been rejected by other banks or had already defaulted and been returned. They were the bottom of the barrel. Yet, Chase was preparing to repackage them, slap a fresh coat of paint on them, and sell them to investors as “Alt-A” securities, a category meant to be far safer than subprime.

The Manicurist and the Magic Numbers

The specific details of the fraud were egregious. When Fleischmann and her team sampled the GreenPoint loans, they found an astronomical defect rate. About 40 percent of the loans were based on overstated incomes. One glaring example involved a manicurist who claimed an annual income of $117,000. Fleischmann did the math: even working seven days a week, the woman would have to work 488 days a year to earn that amount. It was a mathematical impossibility.

Chase’s standard tolerance for error was five percent. This pool was eight times that limit. But when Fleischmann raised the alarm, the pressure from above intensified. The diligence managers began changing their reports. It was a process of coercion; managers were berated until they produced the desired data.

In a pivotal meeting on December 15, 2006, a Chase sales executive pressured the diligence team to clear the loans. Fleischmann watched as a colleague, shaking his head “no,” verbally said “yes” to clearing the impossible loan for the manicurist. Suddenly, the error rate in the pool magically dropped below 10 percent.

Fleischmann refused to stay silent. She approached a managing director, Greg Boester, warning him that selling these high-risk loans as low-risk securities without disclosure would constitute fraud. “You can’t securitize these loans without special disclosure about what’s wrong with them,” she told him. Her warning was ignored. The bank knowingly peddled the toxic product to investors. She later sent a detailed letter—nicknamed “The Howler”—to another managing director, outlining the breakdown in diligence. That letter, too, failed to stop the machine.

A Failure of Justice: The Regulatory Cover-Up

Fleischmann was laid off in 2008, just before the market crashed. Years later, investigators came calling, but what followed was a masterclass in regulatory failure. The Securities and Exchange Commission (SEC), often criticized for its “kid-gloves” approach to Wall Street, failed to pursue the massive fraud Fleischmann had witnessed. Instead, they cherry-picked a single, smaller transaction to fine Chase, ignoring the systemic rot involved in the GreenPoint deal.

Hope briefly returned when the U.S. Attorney’s office in Sacramento took up the case. Civil litigators drafted a detailed complaint that would have exposed the fraud in open court. A press conference was scheduled for September 24, 2013, to announce the charges. But it never happened.

In a move that underscores the concept of “Too Big to Jail,” Jamie Dimon personally called Associate Attorney General Tony West to reopen negotiations. Dimon didn’t just call the prosecutor; he called the prosecutor’s boss. The lawsuit was scrapped. The press conference was canceled. The Department of Justice, led by Attorney General Eric Holder, opted for a backroom deal rather than a public trial.

The $9 Billion Hush Money

The resulting settlement was widely reported as $13 billion, hailed by the government as a historic victory. The reality was far more cynical. The deal was structured to allow Chase to bury the evidence and avoid admitted liability.

First, $4 billion of that headline number was “consumer relief”—a figure widely regarded as accounting fiction. This relief often consisted of credits for loans that were already uncollectible, meaning the bank lost nothing it hadn’t already written off. Furthermore, the relief was often paid for by the investors who bought the bad securities, not by the bank itself.

The remaining $9 billion was the price of secrecy. Instead of a detailed legal complaint that would name names and expose specific acts of fraud, Chase signed a vague “Statement of Facts.” This document was so carefully sanitized that it contained almost no actual facts that could be used to hold individuals accountable.

Crucially, the settlement bypassed the judicial system entirely. Holder’s Justice Department did not present the deal to a judge for review, likely because an honest judge would have rejected it as too lenient. By avoiding the courtroom, Chase avoided public scrutiny. They paid a fine, much of which was tax-deductible, and moved on. The bank’s stock price actually soared on the news, adding billions to its market value. Jamie Dimon, the CEO who oversaw the fraud, received a 74 percent raise shortly after.

Alayne Fleischmann’s experience highlights the perilous position of whistleblowers in the corporate world. She was blocked by internal management, ignored by regulators, and ultimately outed in the press without her consent. Yet, without her, the government would have had little leverage.

For those witnessing fraud today, the landscape offers legal pathways to protection and rewards, though navigating them requires expert legal counsel. The Dodd-Frank Wall Street Reform and Consumer Protection Act, passed in the wake of the financial crisis, established a whistleblower program specifically for securities violations.

Under the SEC Whistleblower Law, individuals who voluntarily provide “original information” about a violation of federal securities laws can be eligible for a significant reward. If the information leads to sanctions exceeding $1 million, the whistleblower can receive between 10% and 30% of the total recovery.

What Constitutes a Violation?

Fleischmann’s case involved several key areas that the SEC program targets:

False Financial Statements: Misrepresenting the quality of the loans.

Accounting Fraud: Manipulating error rates and income data.

Investors Sold Inappropriate Products: Selling “scratch and dent” loans as “Alt-A” securities.

Crucially, the law allows whistleblowers to submit information anonymously, provided they are represented by an attorney. This anonymity is a vital shield for employees who, like Fleischmann, fear retaliation or being blacklisted from their industry.

Furthermore, the False Claims Act allows individuals to file “qui tam” lawsuits if they have evidence of fraud against the government. Given that many of these toxic mortgages ended up in government-backed entities or pension funds, this is another powerful tool for accountability. Violators can be liable for three times the government’s damages, and whistleblowers can receive 15 to 30 percent of the recovery.

Implications for the Financial Industry

The resolution of the JPMorgan Chase case sent a chilling message to the financial industry: crime pays, provided you can pay the fine. The settlement formalized a two-tiered justice system where corporate entities can negotiate their way out of criminal liability.

Eric Holder’s doctrine—that prosecutors must be careful not to destabilize large financial institutions—effectively granted immunity to the “Too Big to Fail” banks. By claiming that responsibility in large corporations is “diffuse,” the government provided a blueprint for executives to insulate themselves from the consequences of their employees’ actions, even when, as in Fleischmann’s case, those actions were directed by management.

The victims of this fraud were not just abstract investors. They were pension funds for teachers and firefighters, credit unions, and ordinary homeowners. The “consumer relief” touted in the settlement often failed to reach those who needed it most, serving instead as a public relations victory for the government and a tax write-off for the bank.

Justice Requires a Voice

Alayne Fleischmann’s story is a testament to the power of a single individual’s conscience against a monolithic system. She refused to be complicit in fraud, even when it cost her a career in finance. “The assumption they make is that I won’t blow up my life to do it,” she said. “But they’re wrong about that.”

While the outcome of the Chase settlement was imperfect, Fleischmann’s testimony ensured that the truth did not remain entirely buried. However, her struggle to be heard underscores the necessity of having powerful advocates in your corner.

If you are witnessing fraud, discrimination, or illegal activities in your workplace, you do not have to navigate the legal system alone. The laws regarding whistleblower protections are complex, and the entities you are up against are powerful. Whether it is securities fraud, tax evasion, or employer violations, there are legitimate avenues to report wrongdoing while protecting your identity and your future.

The “Statement of Facts” may have tried to hide the truth, but facts have a way of surfacing when brave individuals step forward. If you have knowledge of corporate malfeasance, secure your rights and seek counsel who understands the high stakes of speaking truth to power.

When Publix Super Markets gained attention recently, it wasn’t for the quality of its groceries or customer service. Instead, the company has been accused of defrauding its own customers through manipulative checkout practices. This case, centered on allegations of fraudulently inflating the weights of food items advertised at discounted prices, highlights the critical importance of class action lawsuits in protecting consumers and holding corporations accountable.

The Allegations Against Publix Super Markets

The lawsuit against Publix Super Markets was filed in the US District Court for the Southern District of Florida by a group of plaintiffs who claim they were overcharged at checkout due to deceptive pricing practices. The complaint alleges that Publix consistently and systematically misweighed its products, such as deli meats, seafood, and produce, resulting in customers paying more than the advertised price.

Understanding Class Action Lawsuits

Class action lawsuits are lawsuits brought on behalf of a large group of people who have suffered similar harm or damages. These individuals may not have been able to bring a case on their own due to limited resources or because their individual claims may not hold much weight against a powerful corporation.

According to the 47-page lawsuit filed in Florida, Publix is accused of falsely inflating the weights of foods sold by weight, including meats, cheeses, and deli items, at the point of sale. The lawsuit alleges that when customers purchase discounted items, Publix’s point-of-sale (POS) system automatically increases the product’s weight, ensuring customers are charged the original, non-sale price.

For example, the plaintiff purchased pork tenderloin advertised at $4.99 per pound with a savings of $2.00 from the original $6.99 per pound price. The product label indicated it weighed 2.83 pounds, which should have cost $14.12. However, the point-of-sale system allegedly increased the weight to 3.96 pounds, ultimately charging the plaintiff $19.78 – a 40% overcharge.

Making matters worse, Publix’s receipts reportedly omit weight details, leaving customers unaware of these discrepancies. This lack of transparency, combined with employees allegedly being incentivized to conceal the practice and dismiss customer complaints, paints a troubling picture of deliberate consumer exploitation.

The Broader Implications for Consumers

This case goes beyond a single instance of overcharges; it reveals fundamental issues in consumer protection and the accountability of large businesses. Here’s why this lawsuit matters to consumers:

Direct Financial Loss

Every dollar matters, especially as grocery prices continue to rise. Publix’s alleged overcharges mean customers are robbed of promised savings and forced to pay more than they bargained for. Multiply this practice across the company’s 1,439 locations, and the financial impact on consumers is staggering.

Deceptive Practices

At its core, the lawsuit raises serious concerns about dishonesty in business. Deceptive practices like inflating weights and misrepresenting discounts undermine consumer trust—not just in one company but in the broader retail industry.

Holding Corporations Accountable

Without mechanisms like class action lawsuits, large corporations could engage in deceptive practices with little fear of repercussions. An individual filing a lawsuit against a conglomerate might lack the resources to make a meaningful impact. However, collective action enables consumers to pool resources and challenge misconduct effectively, leveling the playing field.

Empowering Consumer Awareness

Cases like this shine a light on unethical corporate behavior and encourage consumers to scrutinize their purchases. By reviewing receipts and questioning discrepancies, shoppers can better protect themselves against potential fraud.

Setting Legal Precedents

The outcome of this lawsuit could establish important legal precedents. Should Publix be found liable, it could lead to stricter regulations preventing similar behavior across the retail industry, ensuring better protections for consumers everywhere.

The Power of Class Action Lawsuits

Class action lawsuits like the one against Publix demonstrate their immense value to society. Individually, it may be impractical to sue a major corporation over a relatively small financial loss. However, when consumers unite, they create a powerful force for justice.

Historical cases underscore the significance of these legal actions:

Volkswagen’s $14 Billion Settlement for emissions fraud punished the automaker for deceptive environmental practices.

The Tobacco Master Settlement Agreement imposed crucial regulations on tobacco companies, advancing public health initiatives.

Enron Securities Litigation recovered billions for defrauded shareholders, providing financial relief and setting an example for corporate accountability.

These cases remind us that class actions aren’t just about financial compensation; they’re about ensuring that corporations prioritize ethical practices and consumer trust over profits.

The Role of Consumers Moving Forward

The allegations against Publix serve as a timely reminder for consumers to stay vigilant. Here’s how you can protect yourself:

Review Receipts Thoroughly

Check for discrepancies in pricing and weights, especially for products sold by weight.

Ask Questions

If something doesn’t seem right, inquire with store employees. Request a breakdown of charges if necessary.

Keep an eye on open lawsuits for which you may qualify. Joining a class action is often as simple as submitting a claim.

Justice for Consumers, Accountability for Corporations

If the allegations in the Publix case are proven, the company’s actions wouldn’t just be a breach of consumer trust; they’d reflect deliberate misconduct designed to profit at the expense of everyday shoppers. Class action lawsuits like this one are essential tools to shine a light on such unethical behavior, seek justice for those affected, and push for systemic change.

Consumers work hard for their money and deserve fair treatment from the businesses they support. The Publix lawsuit teaches us the importance of collective action in protecting those rights. Stay vigilant, informed, and ready to stand united when corporate greed threatens your wallet.

When pursuing a class action lawsuit, it’s crucial to have an attorney with a proven track record of success in collective action cases. An experienced class action attorney understands the complexities of these lawsuits and knows how to advocate effectively on behalf of a large group, ensuring the best possible outcome for everyone involved.

On November 8, 2016, the U.S. Supreme Court heard oral argument in a case Helmer Friedman LLP successfully convinced the high court to hear. The case — Lightfoot v. Fannie Mae, Cendant Mortgage Corporation case (14-1055) — concerns whether individual homeowners who have been wrongly or fraudulently foreclosed upon by Fannie Mae have the right to sue the mortgage giant in the state courts.

According to the Supreme Court, approximately 7,000-8,000 petitions for a writ of certiorari are filed each Term and the Court grants and hears oral argument in merely 80 of those cases – about 1%.

If you want to check out our petition for a writ of certiorari which got the ball in motion for this oral argument, you can read it here http://www.helmerfriedman.com/docs/Petition-Writ_Crystal-Lightfoot-v-Cendant-Mortgage.pdf

She tried to stay quiet, she really did. But after eight years of keeping a heavy secret, the day came when Alayne Fleischmann couldn’t take it anymore.

“It was like watching an old lady get mugged on the street,” she says. “I thought, ‘I can’t sit by any longer.'”

Fleischmann is a tall, thin, quick-witted securities lawyer in her late thirties, with long blond hair, pale-blue eyes and an infectious sense of humor that has survived some very tough times. She’s had to struggle to find work despite some striking skills and qualifications, a common symptom of a not-so-common condition called being a whistle-blower.

Fleischmann is the central witness in one of the biggest cases of white-collar crime in American history, possessing secrets that JPMorgan Chase CEO Jamie Dimon late last year paid $9 billion (not $13 billion as regularly reported – more on that later) to keep the public from hearing.

Back in 2006, as a deal manager at the gigantic bank, Fleischmann first witnessed, then tried to stop, what she describes as “massive criminal securities fraud” in the bank’s mortgage operations.

Thanks to a confidentiality agreement, she’s kept her mouth shut since then. “My closest family and friends don’t know what I’ve been living with,” she says. “Even my brother will only find out for the first time when he sees this interview.”

Six years after the crisis that cratered the global economy, it’s not exactly news that the country’s biggest banks stole on a grand scale. That’s why the more important part of Fleischmann’s story is in the pains Chase and the Justice Department took to silence her.

She was blocked at every turn: by asleep-on-the-job regulators like the Securities and Exchange Commission, by a court system that allowed Chase to use its billions to bury her evidence, and, finally, by officials like outgoing Attorney General Eric Holder, the chief architect of the crazily elaborate government policy of surrender, secrecy and cover-up. “Every time I had a chance to talk, something always got in the way,” Fleischmann says.

This past year she watched as Holder’s Justice Department struck a series of historic settlement deals with Chase, Citigroup and Bank of America. The root bargain in these deals was cash for secrecy. The banks paid big fines, without trials or even judges – only secret negotiations that typically ended with the public shown nothing but vague, quasi-official papers called “statements of facts,” which were conveniently devoid of anything like actual facts.

And now, with Holder about to leave office and his Justice Department reportedly wrapping up its final settlements, the state is effectively putting the finishing touches on what will amount to a sweeping, industry-wide effort to bury the facts of a whole generation of Wall Street corruption. “I could be sued into bankruptcy,” she says. “I could lose my license to practice law. I could lose everything. But if we don’t start speaking up, then this really is all we’re going to get: the biggest financial cover-up in history.”

Alayne Fleischmann grew up in Terrace, British Columbia, a snowbound valley town just a brisk 18-hour drive north of Vancouver. She excelled at school from a young age, making her way to Cornell Law School and then to Wall Street. Her decision to go into finance surprised those closest to her, as she had always had more idealistic ambitions. “I helped lead a group that wrote briefs to the Human Rights Chamber for those affected by ethnic cleansing in Bosnia-Herzegovina,” she says. “My whole life prior to moving into securities law was human rights work.”

But she had student loans to pay off, and so when Wall Street came knocking, that was that. But it wasn’t like she was dragged into high finance kicking and screaming. She found she had a genuine passion for securities law and felt strongly she was doing a good thing. “There was nothing shady about the field back then,” she says. “It was very respectable.”

In 2006, after a few years at a white-shoe law firm, Fleischmann ended up at Chase. The mortgage market was white-hot. Banks like Chase, Bank of America and Citigroup were furiously buying up huge pools of home loans and repackaging them as mortgage securities. Like soybeans in processed food, these synthesized financial products wound up in everything, whether you knew it or not: your state’s pension fund, another state’s workers’ compensation fund, maybe even the portfolio of the insurance company you were counting on to support your family if you got hit by a bus.

As a transaction manager, Fleischmann functioned as a kind of quality-control officer. Her main job was to help make sure the bank didn’t buy spoiled merchandise before it got tossed into the meat grinder and sold out the other end.

A few months into her tenure, Fleischmann would later testify in a DOJ deposition, the bank hired a new manager for diligence, the group in charge of reviewing and clearing loans. Fleischmann quickly ran into a problem with this manager, technically one of her superiors. She says he told her and other employees to stop sending him e-mails. The department, it seemed, was wary of putting anything in writing when it came to its mortgage deals.

“I could lose everything. But if we don’t start speaking up, we’re going to get the biggest financial cover-up in history.”

“If you sent him an e-mail, he would actually come out and yell at you,” she recalls. “The whole point of having a compliance and diligence group is to have policies that are set out clearly in writing. So to have exactly the opposite of that – that was very worrisome.” One former high-ranking federal prosecutor said that if he were taking a criminal case to trial, the information about this e-mail policy would be crucial. “I would begin and end my opening statement with that,” he says. “It shows these people knew what they were doing and were trying not to get caught.”

In late 2006, not long after the “no e-mail” policy was implemented, Fleischmann and her group were asked to evaluate a packet of home loans from a mortgage originator called GreenPoint that was collectively worth about $900 million. Almost immediately, Fleischmann and some of the diligence managers who worked alongside her began to notice serious problems with this particular package of loans.

For one thing, the dates on many of them were suspiciously old. Normally, banks tried to turn loans into securities at warp speed. The idea was to go from a homeowner signing on the dotted line to an investor buying that loan in a pool of securities within two to three months. Thus it was a huge red flag to see Chase buying loans that were already seven or eight months old.

What this meant was that many of the loans in the GreenPoint deal had either been previously rejected by Chase or another bank, or were what are known as “early payment defaults.” EPDs are loans that have already been sold to another bank and have been returned after the borrowers missed multiple payments. That’s why the dates on them were so old.

In other words, this was the very bottom of the mortgage barrel. They were like used cars that had been towed back to the lot after throwing a rod. The industry had its own term for this sort of loan product: scratch and dent. As Chase later admitted, it not only ended up reselling hundreds of millions of dollars worth of those crappy loans to investors, it also sold them in a mortgage pool marketed as being above subprime, a type of loan called “Alt-A.” Putting scratch-and-dent loans in an Alt-A security is a little like putting a fresh coat of paint on a bunch of junkyard wrecks and selling them as new cars. “Everything that I thought was bad at the time,” Fleischmann says, “turned out to be a million times worse.” (Chase declined to comment for this article.)

When Fleischmann and her team reviewed random samples of the loans, they found that around 40 percent of them were based on overstated incomes – an astronomically high defect rate for any pool of mortgages; Chase’s normal tolerance for error was five percent. One mortgage in particular that sticks out in Fleischmann’s mind involved a manicurist who claimed to have an annual income of $117,000. Fleischmann figured that even working seven days a week, this woman would have needed to work 488 days a year to make that much. “And that’s with no overhead,” Fleischmann says. “It wasn’t possible.”

But when she and others raised objections to the toxic loans, something odd started happening. The number-crunchers who had been complaining about the loans suddenly began changing their reports. The process she describes is strikingly similar to the way police obtain false confessions: The interrogator verbally abuses the target until he starts producing the desired answers. “What happened,” Fleischmann says, “is the head diligence manager started yelling at his team, berating them, making them do reports over and over, keeping them late at night.” Then the loans started clearing.

As late as December 11th, 2006, diligence managers had marked a full 33 percent of one loan sample as “stated income unreasonable for profession,” meaning that it was nearly inevitable that there would be a high number of defaults. Several high-ranking executives were copied on this report.

Then, on December 15th, a Chase sales executive held a lengthy meeting with reps from GreenPoint and the diligence team to examine the remaining loans in the pool. When they got to the manicurist, Fleischmann remembers, one of the diligence guys finally caved under the pressure from the sales executive. “He had his hands up and just said, ‘OK,’ and he cleared it,” says Fleischmann, adding that he was shaking his head “no” even as he was saying yes. Soon afterward, the error rate in the pool had magically dropped below 10 percent – a threshold that itself had just been doubled to clear the way for this deal.

After that meeting, Fleischmann testified, she approached a managing director named Greg Boester and pleaded with him to reconsider. She says she told Boester that the bank could not sell the high-risk loans as low-risk securities without committing fraud. “You can’t securitize these loans without special disclosure about what’s wrong with them,” Fleischmann told him, “and if you make that disclosure, no one will buy them.”

A former Olympic ski jumper, Boester was such an important executive at Chase that when he later defected to the Chicago-based hedge fund Citadel, Dimon cut off trading with Citadel in retaliation. Boester eventually returned to Chase and is still there today despite his role in this affair.

This moment illustrates the most basic element of the case against Chase: The bank knowingly peddled products stuffed with scratch-and-dent loans to investors without disclosing the obvious defects with the underlying loans.

Years later, in its settlement with the Justice Department, Chase would admit that this conversation between Fleischmann and Boester took place (though neither was named; it was simply described as “an employee...told...a managing director”) and that her warning was ignored when the bank sold those loans off to investors.

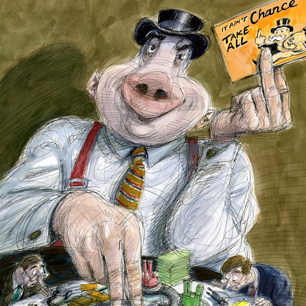

Photo: Illustration by Victor Juhasz

A few weeks later, in early 2007, she sent a long letter to another managing director, William Buell. In the letter, she warned Buell of the consequences of reselling these bad loans as securities and gave detailed descriptions of breakdowns in Chase’s diligence process.

Fleischmann assumed this letter, which Chase lawyers would later jokingly nickname “The Howler” after the screaming missive from the Harry Potter books, would be enough to force the bank to stop selling the bad loans. “It used to be if you wrote a memo, they had to stop, because now there’s proof that they knew what they were doing,” she says. “But when the Justice Department doesn’t do anything, that stops being a deterrent. I just didn’t know that at the time.”

In February 2008, less than two years after joining the bank, Fleischmann was quietly dismissed in a round of layoffs. A few months later, proof would appear that her bosses knew all along that the boom-era mortgage market was rotten. That September, as the market was crashing, Dimon boasted in a ball-washing Fortune article titled “Jamie Dimon’s SWAT Team” that he knew well before the meltdown that the subprime market was toast. “We concluded that underwriting standards were deteriorating across the industry.” The story tells of Dimon ordering Boester’s boss, William King, to dump the bank’s subprime holdings in October 2006. “Billy,” Dimon says, “we need to sell a lot of our positions....This stuff could go up in smoke!”

In other words, two full months before the bank rammed through the dirty GreenPoint deal over Fleischmann’s objections, Chase’s CEO was aware that loans like this were too dangerous for Chase itself to own. (Though Dimon was talking about subprime loans and GreenPoint was technically an Alt-A pool, the Fortune story shows that upper management had serious concerns about industry-wide underwriting problems.)

The ordinary citizen who is the target of a government investigation cannot pick up the phone, call the prosecutor and have his case dropped. But Dimon did just that.

In January 2010, when Dimon testified before the Financial Crisis Inquiry Commission, he told investigators the exact opposite story, portraying the poor Chase leadership as having been duped, just like the rest of us. “In mortgage underwriting,” he said, “somehow we just missed, you know, that home prices don’t go up forever.”

When Fleischmann found out about all of this years later, she was shocked. Her confidentiality agreement at Chase didn’t bar her from reporting a crime, but the problem was that she couldn’t prove that Chase had committed a crime without knowing whether those bad loans had been sold.

As it turned out, of course, Chase was selling those rotten dog-meat loans all over the place. How bad were they? A single lawsuit by a single angry litigant gives some insight. In 2011, Chase was sued over massive losses suffered by a group of credit unions. One of them had invested $135 million in one of the bank’s mortgage–backed securities. About 40 percent of the loans in that deal came from the GreenPoint pool.

The lawsuit alleged that in just the first year, the security suffered $51 million in losses, nearly 50 times what had been projected. It’s hard to say how much of that was due to the GreenPoint loans. But this was just one security, one year, and the losses were in the tens of millions. And Chase did deal after deal with the same methodology. So did most of the other banks. It’s theft on a scale that blows the mind.

In the spring of 2012, Fleischmann, who’d moved back to Canada after leaving Chase, was working at a law firm in Calgary when the phone rang. It was an investigator from the States. “Hi, I’m from the SEC,” he said. “You weren’t expecting to hear from me, were you?”

A few months earlier, President Obama, giving in to pressure from the Occupy movement and other reformers, had formed the Residential Mortgage-Backed Securities Working Group. At least superficially, this was a serious show of force against banks like Chase. The group would operate like a kind of regulatory Justice League, combining the superpowers of investigators from the SEC, the FBI, the IRS, HUD and a host of other federal agencies. It included noted anti-corruption- investigator and New York Attorney General Eric Schneiderman, which gave many observers reason to hope that finally something would be done about the crimes that led to the crash. That makes the fact that the bank would skate with negligible cash fines an even more extra-ordinary accomplishment.

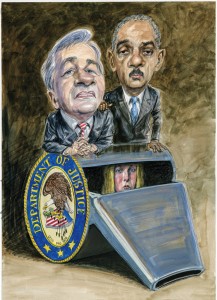

New York Attorney General Eric Schneiderman (L) speaks while Attorney General Eric Holder listens during a news conference at the Justice Department on January 27th, 2012. (Photo: Mark Wilson/Getty)

By the time the working group was set up, most of the applicable statutes of limitations had either expired or were about to expire. “A conspiratorial way of looking at it would be to say the state waited far too long to look at these cases and is now taking its sweet time investigating, while the last statutes of limitations run out,” says famed prosecutor and former New York Attorney General Eliot Spitzer.

It soon became clear that the SEC wasn’t so much investigating Chase’s behavior as just checking boxes. Fleischmann received no follow-up phone calls, even though she told the investigator that she was willing to tell the SEC everything she knew about the systemic fraud at Chase. Instead, the SEC focused on a single transaction involving a mortgage company called WMC. “I kept trying to talk to them about GreenPoint,” Fleischmann says, “but they just wanted to talk about that other deal.”

The following year, the SEC would fine Chase $297 million for misrepresentations in the WMC deal. On the surface, it looked like a hefty punishment. In reality, it was a classic example of the piecemeal, cherry-picking style of justice that characterized the post-crisis era. “The kid-gloves approach that the DOJ and the SEC take with Wall Street is as inexplicable as it is indefensible,” says Dennis Kelleher of the financial reform group Better Markets, which would later file suit challenging the Chase settlement. “They typically charge only one offense when there are dozens. It would be like charging a serial murderer with a single assault and giving them probation.”

Soon Fleischmann’s hopes were raised again. In late 2012 and early 2013, she had a pair of interviews with civil litigators from the U.S. attorney’s office in the Eastern District of California, based in Sacramento.

One of the ongoing myths about the financial crisis is that the government is outmatched by the legal talent representing the banks. But Fleischmann was impressed by the lead attorney in her case, a litigator named Richard Elias. “He sounded like he had been a securities lawyer for 10 years,” she says. “This actually looked like his idea of fun – like he couldn’t wait to run with this case.”

She gave Elias and his team detailed information about everything she’d seen: the edict against e-mails, the sabotaging of the diligence process, the bullying, the written warnings that were ignored, all of it. She assumed that it wouldn’t be long before the bank was hauled into court.

Instead, the government decided to help Chase bury the evidence. It began when Holder’s office scheduled a press conference for the morning of September 24th, 2013, to announce sweeping civil-fraud charges against the bank, all laid out in a detailed complaint drafted by the U.S. attorney’s Sacramento office. But that morning the presser was suddenly canceled, and no complaint was filed. According to later news reports, Dimon had personally called Associate Attorney General Tony West, the third-ranking official in the Justice Department, and asked to reopen negotiations to settle the case out of court.

It goes without saying that the ordinary citizen who is the target of a government investigation cannot simply pick up the phone, call up the prosecutor in charge of his case and have a legal proceeding canceled. But Dimon did just that. “And he didn’t just call the prosecutor, he called the prosecutor’s boss,” Fleischmann says. According to The New York Times, after Dimon had already offered $3 billion to settle the case and was turned down, he went to Holder’s office and upped the offer, but apparently not by enough.

A few days later, Fleischmann, who had by then moved back to Vancouver and was looking for work, was at a mall when she saw a Wall Street Journal headline on her iPhone: JPMorgan Insider Helps U.S. in Probe. The story said that the government had a key witness, a female employee willing to provide damaging testimony about Chase’s mortgage operations. Fleischmann was stunned. Until that moment, she had no idea that she was a major part of the government’s case against Chase. And worse, nobody had bothered to warn her that she was about to be effectively outed in the newspapers. “The stress started to build after I saw that news,” she says. “Especially as I waited to see if my name would come out and I watched my job possibilities evaporate.”

Fleischmann later realized that the government wasn’t interested in having her testify against Chase in court or any other public forum. Instead, the Justice Department’s political wing, led by Holder, appeared to be using her, and her evidence, as a bargaining chip to extract more hush money from Dimon. It worked. Within weeks, Dimon had upped his offer to roughly $9 billion.

In late November, the two sides agreed on a settlement deal that covered a variety of misbehaviors, including the fraud that Fleischmann witnessed as well as similar episodes at Washington Mutual and Bear Stearns, two companies that Chase had acquired during the crisis (with federal bailout aid). The newspapers and the Justice Department described the deal as a “$13 billion settlement,” hailing it as the biggest white-collar regulatory settlement in American history. The deal released Chase from civil liability. And, in what was described by The New York Times as a “major victory for the government,” it left open the possibility that the Justice Department could pursue a further criminal investigation against the bank.

But the idea that Holder had cracked down on Chase was a carefully contrived fiction, one that has survived to this day. For starters, $4 billion of the settlement was largely an accounting falsehood, a chunk of bogus “consumer relief” added to make the payoff look bigger. What the public never grasped about these consumer–relief deals is that the “relief” is often not paid by the bank, which mostly just services the loans, but by the bank’s other victims, i.e., the investors in their bad mortgage securities.

Moreover, in this case, a fine-print addendum indicated that this consumer relief would be allowed only if said investors agreed to it – or if it would have been granted anyway under existing arrangements. This often comes down to either forgiving a small portion of a loan or giving homeowners a little extra time to pay up in full. “It’s not real,” says Fleischmann. “They structured it so that the homeowners only get relief if they would have gotten it anyway.” She pauses. “If a loan shark gives you a few extra weeks to pay up, is that ‘consumer relief’?”

The average person had no way of knowing what a terrible deal the Chase settlement was for the country. The terms were even lighter than the slap-on-the-wrist formula that allowed Wall Street banks to “neither admit nor deny” wrongdoing – the deals that had helped spark the Occupy protests. Yet those notorious deals were like the Nuremberg hangings compared to the regulatory innovation that Holder’s Justice Department cooked up for Dimon and Co.

Instead of a detailed complaint naming names, Chase was allowed to sign a flimsy, 10-and-a-half-page “statement of facts” that was: (a) so short, a first-year law student could read it in the time it takes to eat a tuna sandwich, and (b) so vague, a halfway intelligent person could read it and not know anyone had done anything wrong.

The ink was barely dry on the deal before Chase would have the balls to insinuate its innocence. “The firm has not admitted to violations of the law,” said CFO Marianne Lake. But the deal’s most brazen innovation was the way it bypassed the judicial branch. Previously, federal regulators had had bad luck with judges when trying to dole out slap-on-the-wrist settlements to banks. In a pair of celebrated cases, an unpleasantly honest federal judge named Jed Rakoff had rejected sweetheart deals worked out between banks and slavish regulators and had commanded the state to go back to the drawing board and come up with real punishments.

Seemingly not wanting to deal with even the possibility of such a thing happening, Holder blew off the idea of showing the settlement to a judge. The settlement, says Kelleher, “was unprecedented in many ways, including being very carefully crafted to bypass the court system....There can be little doubt that the DOJ and JP-Morgan were trying to avoid disclosure of their dirty deeds and prevent public scrutiny of their sweetheart deal.” Kelleher asks a rhetorical question: “Can you imagine the outcry if [Bush-era Attorney General] Alberto Gonzales had gone into the backroom and given Halliburton immunity in exchange for a billion dollars?”

The deal was widely considered a good one for both sides, but Chase emerged with barely a scratch. First, the ludicrously nonspecific language surrounding the settlement put you, me and every other American taxpayer on the hook for roughly a quarter of Chase’s check. Because most of the settlement monies were specifically not called fines or penalties, Chase was allowed to treat some $7 billion of the settlement as a tax write-off.

Couple this with the fact that the bank’s share price soared six percent on news of the settlement, adding more than $12 billion in value to shareholders, and one could argue Chase actually made money from the deal. What’s more, to defray the cost of this and other fines, Chase last year laid off 7,500 lower-level employees. Meanwhile, per-employee compensation for everyone else rose four percent, to $122,653. But no one made out better than Dimon. The board awarded a 74 percent raise to the man who oversaw the biggest regulatory penalty ever, upping his compensation package to about $20 million.

“The assumption they make is that I won’t blow up my life to do it. But they’re wrong about that.”

While Holder was being lavishly praised for releasing Chase only from civil liability, Fleischmann knew something the rest of the world did not: The criminal investigation was going nowhere.

In the days leading up to Holder’s November 19th announcement of the settlement, the Justice Department had asked Fleischmann to meet with criminal investigators. They would interview her very soon, they said, between December 15th and Christmas.

But December came and went with no follow-up from the DOJ. She began to wonder: If she was the government’s key witness, how was it possible that they were still pursuing a criminal case without talking to her? “My concern,” she says, “was that they were not investigating.”

The government’s failure to speak to Fleischmann lends credence to a theory about the Holder-Dimon settlement: It included a tacit agreement from the DOJ not to pursue criminal charges in earnest. It sounds outrageous, but it wouldn’t be the first time that the government used a wink and a nod to dispose a bank of major liability without saying so publicly. Back in 2010, American Lawyer revealed Goldman Sachs wanted a full release from liability in a dozen crooked mortgage deals, while the SEC didn’t want to give the bank such a big public victory. So the two sides quietly agreed to a grimy compromise: Goldman agreed to pay $550 million to settle a single case, and the SEC privately assured the bank that it wouldn’t recommend charges in any of the other deals.

As Fleischmann was waiting for the Justice Department to call, Chase and its lawyers had been going to tremendous lengths to keep her muzzled. A number of major institutional investors had sued the bank in an effort to recover money lost in investing in Chase’s fraud-ridden home loans. In October 2013, one of those investors – the Fort Worth Employees’ Retirement Fund – asked a federal judge to force Chase to grant access to a series of current and former employees, including Fleischmann, whose status as a key cooperator in the federal investigation had made headlines in The Wall Street Journal and other major media outlets.

Photo: Spencer Platt/Getty

In response, Dorothy Spenner, an attorney representing Chase, told the court that Fleischmann was not a “relevant custodian.” In other words, she couldn’t testify to anything of importance. Federal Magistrate Judge James C. Francis IV took Chase’s lawyers at their word and rejected the Fort Worth retirees’ request for access to Fleischmann and her evidence.

Other investors bilked by Chase also tried to speak to Fleischmann. The Federal Home Loan Bank of Pittsburgh, which had sued Chase, asked the court to force Chase to turn over a copy of the draft civil complaint that was withheld after Holder’s scuttled press conference. The Pittsburgh litigants also specified that they wanted access to the name of the state’s cooperating witness: namely, Fleischmann.

In that case, the judge actually ordered Chase to turn over both the complaint and Fleischmann’s name. Chase stalled. Later in the fall, the judge ordered the bank to produce the information again; it stalled some more.

Then, in January 2014, Chase suddenly settled with the Pittsburgh bank out of court for an undisclosed amount. Months after being ordered to allow Fleischmann to talk, they once again paid a stiff price to keep her testimony out of the public eye.

Chase’s determination to hide its own dirt while forcing Fleischmann to keep her secret was becoming more and more absurd. “It was a hard time to look for work,” she says. All that prospective employers knew was that she had worked in a department that had just been dinged with what was then the biggest regulatory fine in the history of capitalism. According to the terms of her confidentiality agreement, she couldn’t even tell them that she’d tried to keep the bank from committing fraud.

Despite it all, Fleischmann still had faith that the Justice Department or some other federal agency would make things right. “I guess I was just a trusting person,” she says. “I wasn’t cynical. I kept hoping.”

One day last spring, Fleischmann happened across a video of Holder giving a speech titled “No Company Is Too Big to Jail.” It was classic Holder: full of weird prevarication, distracting eye twitches and other facial contortions. It began with the bold rejection of the idea that overly large financial institutions would receive preferential treatment from his Justice Department.

Then, within a few sentences, he seemed to contradict himself, arguing that one must apply a special sort of care when investigating supersize banks, tweaking the rules so as not to upset the world economy. “Federal prosecutors conducting these investigations,” Holder said, “must go the extra mile to coordinate closely with the regulators who oversee these institutions’ day-to-day operations.” That is, he was saying, regulators have to agree not to allow automatic penalties to kick in, so that bad banks can stay in business.

Fleischmann winced. Fully fluent in Holder’s three-faced rhetoric after years of waiting for him to act, she felt that he was patting himself on the back for having helped companies survive crimes that otherwise might have triggered crippling regulatory penalties. As she watched in mounting outrage, Holder wrapped up his address with a less-than-reassuring pronouncement: “I am resolved to seeing [the investigations] through.” Doing so, he added, would “reaffirm” his principles.

Or, as Fleischmann translates it: “I will personally stay on to make sure that no one can undo the cover-up that I’ve accomplished.”

That’s when she decided to break her silence. “I tried to go on with the things I was doing, but I just stopped sleeping and couldn’t eat,” she says. “It felt like I was trying to keep this secret and my body was literally rejecting it.”

Ironically, over the summer, the government contacted her again. A new set of investigators interviewed her, appearing to have restarted the criminal case. Fleischmann won’t comment on that investigation. Frustrated as she has been by the decisions of the higher-ups in Holder’s Justice Department, she doesn’t want to do anything to get in the way of investigators who might be working the case. But she emphasizes she still has reason to be deeply worried that nothing will be done. Even if the investigators build strong cases against executives who oversaw Chase’s fraud, Holder or whoever succeeds him can still make the whole thing disappear by negotiating a soft landing for the company. “That’s the thing I’m worried about,” she says. “That they make the whole thing disappear. If they do that, the truth will never come out.”

In September, at a speech at NYU, Holder defended the lack of prosecutions of top executives on the grounds that, in the corporate context, sometimes bad things just happen without actual people being responsible. “Responsibility remains so diffuse, and top executives so insulated,” Holder said, “that any misconduct could again be considered more a symptom of the institution’s culture than a result of the willful actions of any single individual.”

In other words, people don’t commit crimes, corporate culture commits crimes! It’s probably fortunate that Holder is quitting before he has time to apply the same logic to Mafia or terrorism cases.

Fleischmann, for her part, had begun to find the whole situation almost funny.

“I thought, ‘I swear, Eric Holder is gas-lighting me,’ ” she says.

Ask her where the crime was, and Fleischmann will point out exactly how her bosses at JPMorgan Chase committed criminal fraud: It’s right there in the documents; just hand her a highlighter and some Post-it notes – “We lawyers love flags” – and you will not find a more enthusiastic tour guide through a gazillion-page prospectus than Alayne Fleischmann.

She believes the proof is easily there for all the elements of the crime as defined by federal law – the bank made material misrepresentations, it made material omissions, and it did so willfully and with specific intent, consciously ignoring warnings from inside the firm and out.

She’d like to see something done about it, emphasizing that there still is time. The statute of limitations for wire fraud, for instance, has not run out, and she strongly believes there’s a case there, against the bank’s executives. She has no financial interest in any of this, no motive other than wanting the truth out. But more than anything, she wants it to be over.

In today’s America, someone like Fleischmann – an honest person caught for a little while in the wrong place at the wrong time – has to be willing to live through an epic ordeal just to get to the point of being able to open her mouth and tell a truth or two. And when she finally gets there, she still has to risk everything to take that last step. “The assumption they make is that I won’t blow up my life to do it,” Fleischmann says. “But they’re wrong about that.”

Good for her, and great for her that it’s finally out. But the big-picture ending still stings. She hopes otherwise, but the likely final verdict is a Pyrrhic victory.

Because after all this activity, all these court actions, all these penalties (both real and abortive), even after a fair amount of noise in the press, the target companies remain more ascendant than ever. The people who stole all those billions are still in place. And the bank is more untouchable than ever – former Debevoise & Plimpton hotshots Mary Jo White and Andrew Ceresny, who represented Chase for some of this case, have since been named to the two top jobs at the SEC. As for the bank itself, its stock price has gone up since the settlement and flirts weekly with five-year highs. They may lose the odd battle, but the markets clearly believe the banks won the war. Truth is one thing, and if the right people fight hard enough, you might get to hear it from time to time. But justice is different, and still far enough away.

On November 8, 2016, the U.S. Supreme Court heard oral argument in a case Helmer Friedman LLP successfully convinced the high court to hear. The case — Lightfoot v. Fannie Mae, Cendant Mortgage Corporation case (14-1055) — concerns whether individual homeowners who have been wrongly or fraudulently foreclosed upon by Fannie Mae have the right to sue the mortgage giant in the state courts.

On November 8, 2016, the U.S. Supreme Court heard oral argument in a case Helmer Friedman LLP successfully convinced the high court to hear. The case — Lightfoot v. Fannie Mae, Cendant Mortgage Corporation case (14-1055) — concerns whether individual homeowners who have been wrongly or fraudulently foreclosed upon by Fannie Mae have the right to sue the mortgage giant in the state courts.